Selling a home involves more than just listing a property. Charlotte-based Clients1st Property Group helps sellers navigate expenses tied to finalizing a real estate transaction. These fees, often ranging from 1-3% of the sale price, cover essential services required to transfer ownership smoothly.

Understanding these expenses is critical for anyone preparing to sell. In Charlotte, North Carolina, common seller obligations include transfer taxes (typically $2 per $1,000 of sale price), escrow fees, and real estate agent commissions. Local expertise matters, as regulations and rates vary by region.

This guide breaks down every fee sellers might encounter, supported by industry data and regional insights. Whether you’re dealing with title insurance requirements or preparing for the final walkthrough, Clients1st Property Group offers tailored support. Their team can be reached at (704) 622-4865 for personalized advice.

Both buyers and sellers share responsibilities during this phase. Title searches, document preparation, and prorated property taxes all factor into the equation. By clarifying these elements upfront, homeowners gain confidence in their financial planning.

Key Takeaways

- Sellers typically cover fees like transfer taxes and agent commissions

- Total expenses often range between 1-3% of the home’s sale price

- Charlotte-specific regulations impact cost calculations

- Title-related services ensure legal ownership transfer

- Local experts provide critical guidance for smooth transactions

- Contact Clients1st at (704) 622-4865 for personalized support

Introduction to Closing Costs for Sellers

Homeowners often face unexpected charges when completing a real estate deal. These transaction-related expenses, commonly called closing costs, cover services required to legally transfer property ownership. In Charlotte, fees typically split between both parties, but sellers carry specific obligations influenced by local regulations and market dynamics.

Overview of Seller-Related Fees

Sellers primarily handle real estate agent commissions, title insurance, and transfer taxes. While buyers focus on mortgage-related charges, homeowner responsibilities include:

- Agent commissions (5-6% of sale price, usually split between listing and buyer’s agents)

- Title search fees ($200-$400 to verify ownership history)

- Transfer taxes ($2 per $1,000 of sale price in Mecklenburg County)

Additional costs might involve escrow services, prorated property taxes, or HOA dues. Unlike fixed-rate buyer fees, many seller expenses tie directly to the home’s final price.

Why Understanding Closing Costs Matters in Charlotte, NC

Charlotte’s competitive market requires strategic budgeting. Local transfer taxes and title requirements differ from neighboring states, making regional expertise essential. Buyers often negotiate concessions tied to loan approvals, which can shift certain fees to sellers.

Clients1st Property Group emphasizes proactive planning: “Reviewing these expenses early prevents surprises at settlement.” Their team helps homeowners balance percentage-based commissions with fixed legal fees, ensuring sellers retain maximum equity.

For personalized guidance, contact (704) 622-4865. Knowledgeable support transforms complex fee structures into manageable, predictable line items.

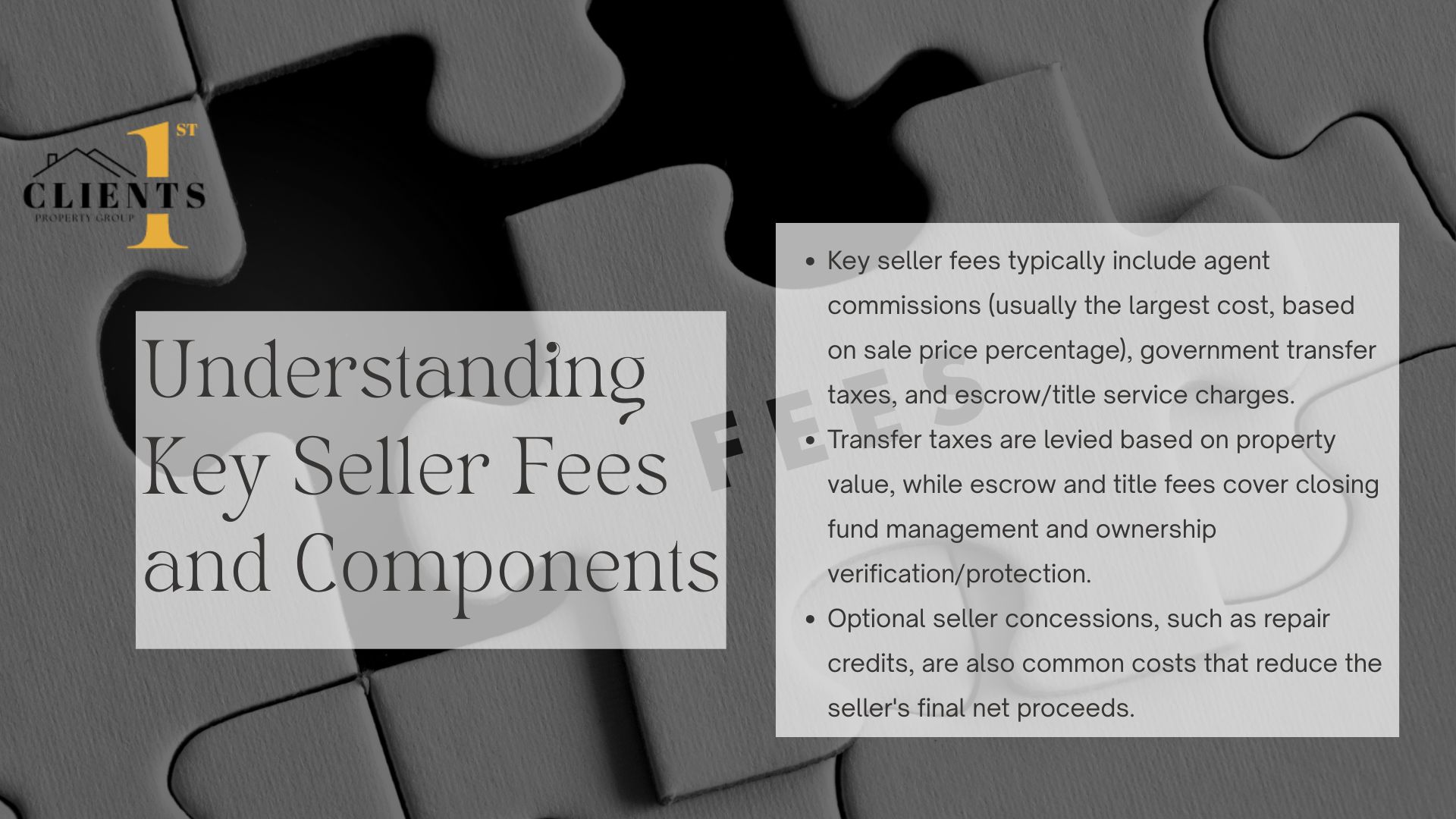

Understanding Key Seller Fees and Components

Finalizing a property sale requires careful financial planning beyond the listing price. Three primary expenses shape sellers’ net proceeds: agent commissions, transfer taxes, and escrow services. Each component ties directly to the transaction’s value and local regulations.

Real Estate Agent Commissions and Seller Concessions

Agent fees typically consume the largest portion of seller expenses. In Charlotte, commissions average 5–6% of the sale price, split between listing and buyer’s agents. For a $400,000 home, this equals $20,000–$24,000. Some brokers offer reduced rates (2.5–3% per agent) in competitive markets.

Seller concessions differ from buyer requests. These voluntary offers might cover repair credits or temporary rate buydowns. While negotiable, they reduce the seller’s final profit margin.

Transfer Taxes, Escrow Fees, and Other Expenses

State and local governments charge transfer taxes to record ownership changes. Mecklenburg County applies a $2 per $1,000 rate—$800 on a $400,000 transaction. Escrow services, managing funds until closing, often cost 1–2% of the sale price.

“Reviewing title reports early prevents last-minute disputes over property boundaries or liens,” advises Clients1st Property Group.

| Fee Type | Average Cost | Calculation Basis |

|---|---|---|

| Agent Commission | 5–6% | Sale Price |

| Transfer Tax | $2/$1,000 | Sale Price |

| Escrow Services | 1–2% | Sale Price |

| Title Insurance | $1,000–$2,500 | Loan Amount |

Title searches verify legal ownership, while insurance protects against future claims. Combined, these services ensure smooth property transfers. Charlotte homeowners should budget $1,500–$3,000 for these protections, depending on the home’s value.

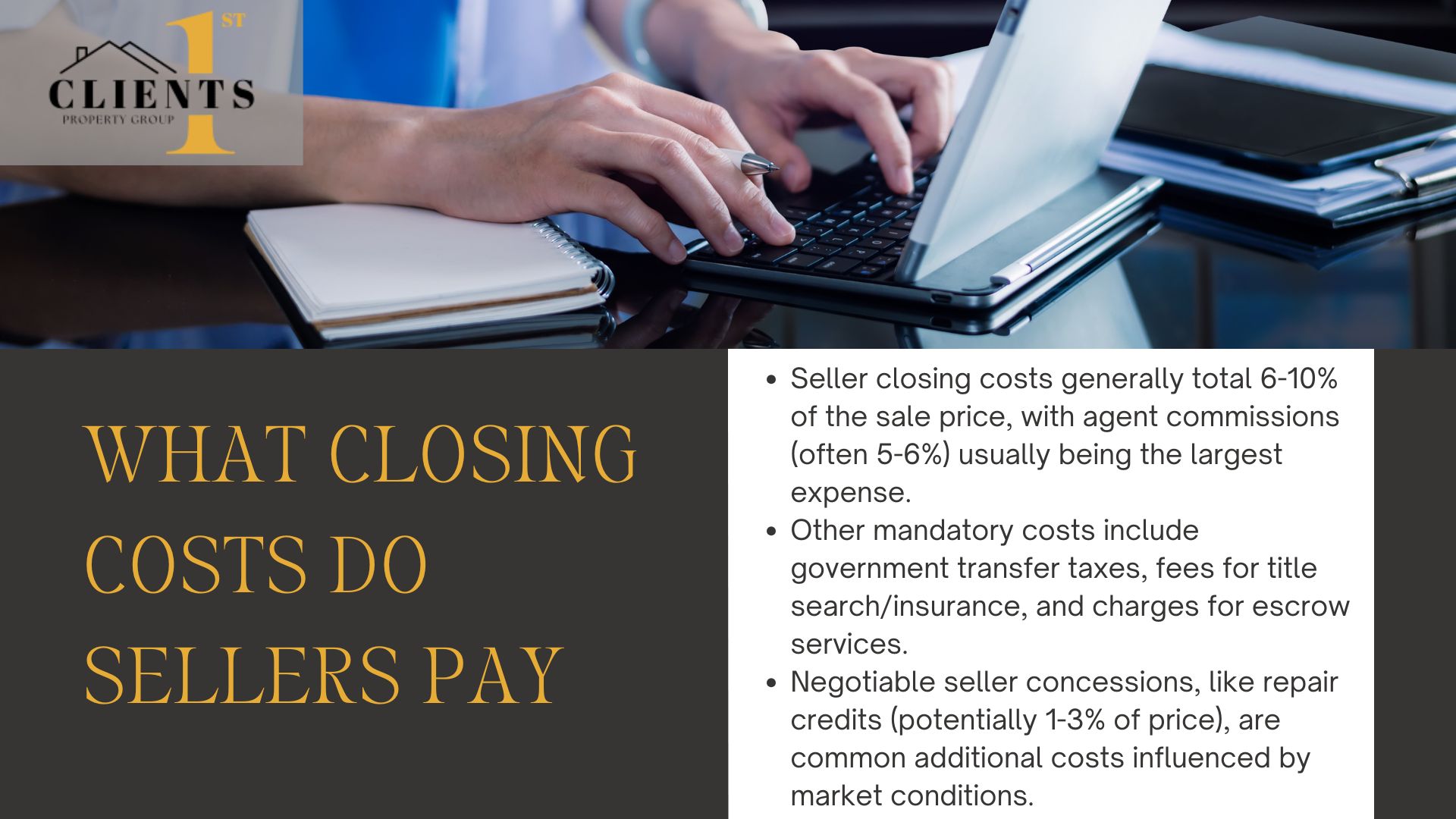

Detailed Analysis: what closing costs do sellers pay

Property transactions reveal layered financial obligations beyond the initial price agreement. A $400,000 home sale in Charlotte typically sees sellers allocating 6–10% of the proceeds to mandatory and negotiable fees. This range accounts for fixed expenses like taxes and variable charges influenced by market conditions.

Breaking Down the Costs in Detail

Commission fees dominate seller expenses, consuming 5–6% of the transaction value. Transfer taxes add $800–$1,200 for mid-priced homes, while title services average $1,800–$2,500. Concessions—like covering inspection repairs—can reduce net proceeds by an additional 1–3%.

| Expense Category | Typical Range | Impact on $400k Sale |

|---|---|---|

| Agent Commissions | 5–6% | $20,000–$24,000 |

| Transfer Taxes | 0.2% | $800 |

| Title Services | 0.45–0.63% | $1,800–$2,500 |

| Seller Concessions | 1–3% | $4,000–$12,000 |

Market dynamics influence these figures significantly. During buyer-favorable conditions, concessions often rise as purchasers request help with rate buydowns or repair credits. Luxury properties frequently incur higher title insurance premiums due to complex ownership histories.

Consider a recent transaction where a seller agreed to 2% concessions. This reduced their $750,000 home proceeds by $15,000—on top of standard fees totaling $48,750. Scrutinizing each line item during disclosure reviews helps identify negotiable charges, particularly with title search providers or escrow companies.

Clients1st Property Group notes: “Every dollar preserved through careful negotiation directly boosts your equity position.” Their specialists routinely save clients 0.5–1.5% through strategic vendor comparisons and concession caps.

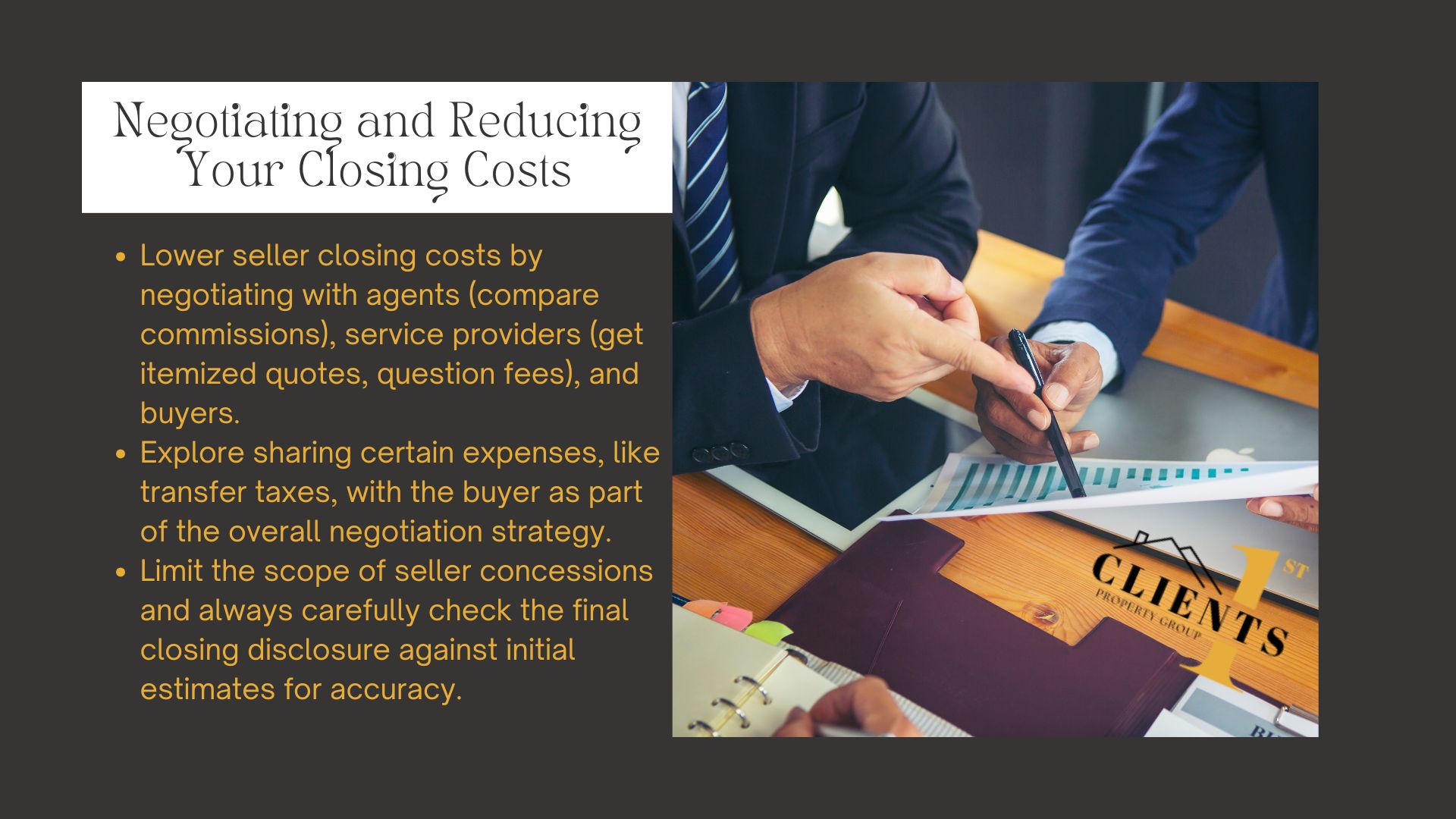

Negotiating and Reducing Your Closing Costs

Smart negotiation strategies can significantly lower expenses during property transactions. While some fees appear fixed, sellers often retain flexibility through informed discussions with buyers and vendors. Proactive planning helps identify areas where adjustments might align with market conditions.

Tips for Negotiating with Buyers and Service Providers

Start by comparing multiple real estate professionals. Discount brokers offering 4% total commissions (vs. the standard 6%) have gained traction in competitive markets like Charlotte. Always request itemized quotes from title companies and attorneys—many reduce administrative fees when asked directly.

Transfer taxes often become negotiation points. In recent transactions, sellers split these costs with buyers by offering a 1% price reduction instead. This approach preserved net proceeds while accommodating purchaser budget constraints.

“Review every line item—title search fees and courier charges sometimes include padding,” advises Clients1st Property Group. “Politely questioning these can yield instant savings.”

Consider these actionable tactics:

- Request flat-rate legal fees instead of hourly billing

- Bundle title insurance with escrow services for package discounts

- Limit concessions to specific items like inspection repairs

Recent trends show sellers saving $2,100–$4,500 by negotiating non-commission expenses. One Charlotte homeowner reduced title search fees by 30% through provider comparisons. Always cross-reference the closing disclosure against initial estimates to catch discrepancies.

Clear communication establishes realistic expectations. State your fee reduction goals early when working with agents and lenders. Many professionals adjust rates to secure listings, especially in slower markets.

Title Insurance, Legal Fees, and Property Transfers

Securing clear property ownership requires precise documentation and protective measures. Title-related services and legal reviews form the backbone of secure real estate transfers, ensuring both parties meet obligations without hidden risks.

Understanding Title Insurance and Title Searches

Title insurance shields homeowners and lenders from unresolved claims or errors in ownership history. Policies come in two forms:

- Owner’s coverage: Protects against past title defects (forged deeds, undisclosed heirs)

- Lender’s policy: Required by mortgage companies, covering loan amounts

Thorough title searches uncover liens, easements, or boundary disputes before finalizing sales. Charlotte agents often recommend budgeting $1,200–$2,800 for these services, depending on property complexity.

Examining Legal Fees and Mortgage Payoffs

Legal expenses vary by state—North Carolina doesn’t mandate attorney involvement, but many sellers hire one for contract reviews. Typical charges include:

| Service | Average Cost | Responsibility |

|---|---|---|

| Deed Preparation | $150–$300 | Seller |

| Closing Coordination | $500–$1,200 | Split |

| Mortgage Payoff Processing | $50–$150 | Seller |

“Review payoff statements early,” advises Clients1st Property Group. “Processing delays can push back settlement dates, incurring extra fees.”

Mortgage payoffs often include prorated interest or prepayment penalties. Sellers should request loan satisfaction statements 30 days before closing to avoid surprises. Comparing attorney rates and bundling services can reduce expenses by 10–15% in competitive markets.

Local Considerations in Charlotte, North Carolina

Regional factors play a decisive role in managing transaction expenses for property owners. Charlotte’s real estate market features unique tax structures and service provider dynamics that directly impact net proceeds. Understanding these local nuances helps owners retain more money while complying with ownership transfer protocols.

Impact of State and Local Transfer Taxes

North Carolina imposes a statewide transfer tax of $2 per $1,000 of sale value. Mecklenburg County adds another $2 per $1,000, doubling the total rate compared to rural areas. For a $400,000 home, this creates a $1,600 expense—40% higher than South Carolina’s blended rate.

| State | Base Rate | County Add-On | Total per $400k |

|---|---|---|---|

| NC | $2/$1k | $2/$1k | $1,600 |

| SC | $1.85/$1k | $0.15/$1k | $800 |

| GA | $1/$1k | Varies | $400–$1,200 |

Charlotte Market Trends and Service Cost Variations

Competitive pricing among local title companies creates opportunities for discounts. Recent data shows title searches averaging $350–$550 in Charlotte versus $600+ in Raleigh. Legal fees also vary widely—some firms charge flat rates of $1,200, while others bill hourly ($200–$300).

Ownership documentation requires precision in fast-moving markets. One homeowner saved $1,100 by comparing three escrow providers before selecting a mid-priced option. Clients1st Property Group advises: “Bundle services with experienced local vendors to balance quality and expenses.”

To navigate these variables, request itemized quotes early. Many providers offer reduced rates for high-value transactions or repeat clients. Strategic planning turns regional challenges into manageable expenses.

Preparing for Closing Day and Final Settlement

Finalizing a real estate transaction demands meticulous preparation across financial and legal fronts. Organizing documents early prevents last-minute scrambles while ensuring all parties meet contractual obligations. Attention to detail during this phase directly impacts how smoothly ownership transfers occur.

Essential Documentation and Check Preparations

Gather these critical items at least three days before settlement:

- Government-issued photo ID for all owners

- Original deed and recent property tax statements

- Mortgage payoff statements with per-diem interest calculations

- Certified checks covering prorated property taxes and agreed concessions

Coordinate with your real estate agent to verify check amounts against the settlement statement. Digital transfers are increasingly common, but many title companies still require certified funds. Double-check payee names and amounts—errors here can delay proceedings by days.

Reviewing the Closing Disclosure

Federal law mandates receiving this document three business days before settlement. Compare it line-by-line with your initial Loan Estimate and final settlement statement. Key areas requiring scrutiny include:

| Section | Verify | Common Errors |

|---|---|---|

| Loan Costs | Matches agreed terms | Incorrect origination fees |

| Taxes | Prorations align with local rates | Overestimated escrow |

| Concessions | Matches contract addendums | Unapproved credits |

Buyer seller agreements often include last-minute adjustments. Ensure sale price modifications and seller concessions appear accurately. One Charlotte homeowner recently caught a $2,800 error in prorated property taxes during this review phase.

Attorneys recommend physically initialing each disclosure page after verification. Keep digital and paper copies for seven years post-transaction. Proactive document management transforms a complex home sale into an organized, predictable process.

Conclusion

Successfully transferring property ownership hinges on understanding key expenses tied to the process. Sellers typically cover costs like agent commissions, transfer taxes, and title services—each influenced by the home’s purchase price. These fees ensure legal compliance while protecting both parties’ interests.

Charlotte’s market adds unique layers, such as local transfer tax rates and competitive title service pricing. Negotiating terms early helps reduce financial surprises, especially when working with experienced professionals. Reviewing every line item in settlement statements ensures fees align with regional standards.

Clients1st Property Group specializes in demystifying these complexities for Charlotte homeowners. Their team’s local expertise helps sellers anticipate expenses tied to the purchase price while identifying savings opportunities. Proactive planning transforms overwhelming fee structures into manageable steps.

For tailored guidance, contact (704) 622-4865. Whether navigating prorated taxes or title searches, detailed preparation paired with expert support maximizes your financial outcomes. Knowledge remains the ultimate tool in achieving smooth, profitable real estate transactions.

Final Thoughts on Closing Costs for Home Sellers in Charlotte

Which fees are sellers typically required to cover during a property transaction?

How do transfer taxes function in North Carolina real estate transactions?

Which fees are sellers typically required to cover during a property transaction?

How do transfer taxes function in North Carolina real estate transactions?

Final Thoughts on Closing Costs for Home Sellers in Charlotte

Which fees are sellers typically required to cover during a property transaction?

Sellers generally pay real estate agent commissions (5-6% of sale price), transfer taxes, title insurance premiums, and prorated property taxes. Additional costs may include attorney fees, escrow charges, and any negotiated concessions like covering buyer’s inspection fees or mortgage discount points.

How do transfer taxes function in North Carolina real estate transactions?

North Carolina imposes a statewide excise tax of

Final Thoughts on Closing Costs for Home Sellers in Charlotte

Which fees are sellers typically required to cover during a property transaction?

Sellers generally pay real estate agent commissions (5-6% of sale price), transfer taxes, title insurance premiums, and prorated property taxes. Additional costs may include attorney fees, escrow charges, and any negotiated concessions like covering buyer’s inspection fees or mortgage discount points.

How do transfer taxes function in North Carolina real estate transactions?

North Carolina imposes a statewide excise tax of $1 per $500 of sale value. Mecklenburg County adds a 0.2% local transfer tax. For a $400,000 home, sellers pay approximately $1,200 in combined state and county transfer taxes at closing.

Can commission rates be negotiated with real estate agents in Charlotte?

Yes. While 6% remains common, many Charlotte agents offer reduced rates (4-5%) for competitive listings or dual-agency situations. Sellers should compare services from firms like Allen Tate and RE/MAX when negotiating terms.

Why does title insurance matter for property transfers?

Title insurance protects against ownership disputes or liens discovered post-sale. Sellers typically pay for the owner’s policy (averaging $1,000-$2,500 in NC), which ensures clear transfer of rights and reduces legal risks for both parties.

How do concessions impact a home sale’s financial outcome?

Seller concessions—like covering repair costs or buyer’s closing fees—lower net proceeds but can expedite sales. In Charlotte’s balanced market, 2-3% concessions are common to offset buyer financing hurdles without drastically affecting final profits.

What documents should Charlotte sellers prepare before settlement?

Essential items include the original deed, property tax receipts, HOA agreements (if applicable), and a paid mortgage statement. Local attorneys like Horack Talley often require a government-issued ID and recent utility bills for residency verification.

Are there strategies to minimize expenses during property transfers?

Sellers can bundle title services with preferred providers, contest high escrow fees, or opt for flat-rate legal assistance. Timing the sale to align with tax proration cycles also helps reduce out-of-pocket costs.

How does paying off an existing loan affect closing settlements?

Mortgage payoffs (including any prepayment penalties) are deducted from sale proceeds. Sellers receive remaining funds after settling balances—a process managed by closing attorneys who coordinate with lenders like Bank of America or Truist.

per 0 of sale value. Mecklenburg County adds a 0.2% local transfer tax. For a 0,000 home, sellers pay approximately

Final Thoughts on Closing Costs for Home Sellers in Charlotte

Which fees are sellers typically required to cover during a property transaction?

Sellers generally pay real estate agent commissions (5-6% of sale price), transfer taxes, title insurance premiums, and prorated property taxes. Additional costs may include attorney fees, escrow charges, and any negotiated concessions like covering buyer’s inspection fees or mortgage discount points.

How do transfer taxes function in North Carolina real estate transactions?

North Carolina imposes a statewide excise tax of $1 per $500 of sale value. Mecklenburg County adds a 0.2% local transfer tax. For a $400,000 home, sellers pay approximately $1,200 in combined state and county transfer taxes at closing.

Can commission rates be negotiated with real estate agents in Charlotte?

Yes. While 6% remains common, many Charlotte agents offer reduced rates (4-5%) for competitive listings or dual-agency situations. Sellers should compare services from firms like Allen Tate and RE/MAX when negotiating terms.

Why does title insurance matter for property transfers?

Title insurance protects against ownership disputes or liens discovered post-sale. Sellers typically pay for the owner’s policy (averaging $1,000-$2,500 in NC), which ensures clear transfer of rights and reduces legal risks for both parties.

How do concessions impact a home sale’s financial outcome?

Seller concessions—like covering repair costs or buyer’s closing fees—lower net proceeds but can expedite sales. In Charlotte’s balanced market, 2-3% concessions are common to offset buyer financing hurdles without drastically affecting final profits.

What documents should Charlotte sellers prepare before settlement?

Essential items include the original deed, property tax receipts, HOA agreements (if applicable), and a paid mortgage statement. Local attorneys like Horack Talley often require a government-issued ID and recent utility bills for residency verification.

Are there strategies to minimize expenses during property transfers?

Sellers can bundle title services with preferred providers, contest high escrow fees, or opt for flat-rate legal assistance. Timing the sale to align with tax proration cycles also helps reduce out-of-pocket costs.

How does paying off an existing loan affect closing settlements?

Mortgage payoffs (including any prepayment penalties) are deducted from sale proceeds. Sellers receive remaining funds after settling balances—a process managed by closing attorneys who coordinate with lenders like Bank of America or Truist.

,200 in combined state and county transfer taxes at closing.

Can commission rates be negotiated with real estate agents in Charlotte?

Yes. While 6% remains common, many Charlotte agents offer reduced rates (4-5%) for competitive listings or dual-agency situations. Sellers should compare services from firms like Allen Tate and RE/MAX when negotiating terms.

Why does title insurance matter for property transfers?

Title insurance protects against ownership disputes or liens discovered post-sale. Sellers typically pay for the owner’s policy (averaging

Final Thoughts on Closing Costs for Home Sellers in Charlotte

Which fees are sellers typically required to cover during a property transaction?

Sellers generally pay real estate agent commissions (5-6% of sale price), transfer taxes, title insurance premiums, and prorated property taxes. Additional costs may include attorney fees, escrow charges, and any negotiated concessions like covering buyer’s inspection fees or mortgage discount points.

How do transfer taxes function in North Carolina real estate transactions?

North Carolina imposes a statewide excise tax of $1 per $500 of sale value. Mecklenburg County adds a 0.2% local transfer tax. For a $400,000 home, sellers pay approximately $1,200 in combined state and county transfer taxes at closing.

Can commission rates be negotiated with real estate agents in Charlotte?

Yes. While 6% remains common, many Charlotte agents offer reduced rates (4-5%) for competitive listings or dual-agency situations. Sellers should compare services from firms like Allen Tate and RE/MAX when negotiating terms.

Why does title insurance matter for property transfers?

Title insurance protects against ownership disputes or liens discovered post-sale. Sellers typically pay for the owner’s policy (averaging $1,000-$2,500 in NC), which ensures clear transfer of rights and reduces legal risks for both parties.

How do concessions impact a home sale’s financial outcome?

Seller concessions—like covering repair costs or buyer’s closing fees—lower net proceeds but can expedite sales. In Charlotte’s balanced market, 2-3% concessions are common to offset buyer financing hurdles without drastically affecting final profits.

What documents should Charlotte sellers prepare before settlement?

Essential items include the original deed, property tax receipts, HOA agreements (if applicable), and a paid mortgage statement. Local attorneys like Horack Talley often require a government-issued ID and recent utility bills for residency verification.

Are there strategies to minimize expenses during property transfers?

Sellers can bundle title services with preferred providers, contest high escrow fees, or opt for flat-rate legal assistance. Timing the sale to align with tax proration cycles also helps reduce out-of-pocket costs.

How does paying off an existing loan affect closing settlements?

Mortgage payoffs (including any prepayment penalties) are deducted from sale proceeds. Sellers receive remaining funds after settling balances—a process managed by closing attorneys who coordinate with lenders like Bank of America or Truist.

,000-,500 in NC), which ensures clear transfer of rights and reduces legal risks for both parties.

How do concessions impact a home sale’s financial outcome?

Seller concessions—like covering repair costs or buyer’s closing fees—lower net proceeds but can expedite sales. In Charlotte’s balanced market, 2-3% concessions are common to offset buyer financing hurdles without drastically affecting final profits.

What documents should Charlotte sellers prepare before settlement?

Essential items include the original deed, property tax receipts, HOA agreements (if applicable), and a paid mortgage statement. Local attorneys like Horack Talley often require a government-issued ID and recent utility bills for residency verification.

Are there strategies to minimize expenses during property transfers?

Sellers can bundle title services with preferred providers, contest high escrow fees, or opt for flat-rate legal assistance. Timing the sale to align with tax proration cycles also helps reduce out-of-pocket costs.

How does paying off an existing loan affect closing settlements?

Mortgage payoffs (including any prepayment penalties) are deducted from sale proceeds. Sellers receive remaining funds after settling balances—a process managed by closing attorneys who coordinate with lenders like Bank of America or Truist.

Final Thoughts on Closing Costs for Home Sellers in Charlotte

Which fees are sellers typically required to cover during a property transaction?

Sellers generally pay real estate agent commissions (5-6% of sale price), transfer taxes, title insurance premiums, and prorated property taxes. Additional costs may include attorney fees, escrow charges, and any negotiated concessions like covering buyer’s inspection fees or mortgage discount points.

How do transfer taxes function in North Carolina real estate transactions?

North Carolina imposes a statewide excise tax of

Final Thoughts on Closing Costs for Home Sellers in Charlotte

Which fees are sellers typically required to cover during a property transaction?

Sellers generally pay real estate agent commissions (5-6% of sale price), transfer taxes, title insurance premiums, and prorated property taxes. Additional costs may include attorney fees, escrow charges, and any negotiated concessions like covering buyer’s inspection fees or mortgage discount points.

How do transfer taxes function in North Carolina real estate transactions?

North Carolina imposes a statewide excise tax of $1 per $500 of sale value. Mecklenburg County adds a 0.2% local transfer tax. For a $400,000 home, sellers pay approximately $1,200 in combined state and county transfer taxes at closing.

Can commission rates be negotiated with real estate agents in Charlotte?

Yes. While 6% remains common, many Charlotte agents offer reduced rates (4-5%) for competitive listings or dual-agency situations. Sellers should compare services from firms like Allen Tate and RE/MAX when negotiating terms.

Why does title insurance matter for property transfers?

Title insurance protects against ownership disputes or liens discovered post-sale. Sellers typically pay for the owner’s policy (averaging $1,000-$2,500 in NC), which ensures clear transfer of rights and reduces legal risks for both parties.

How do concessions impact a home sale’s financial outcome?

Seller concessions—like covering repair costs or buyer’s closing fees—lower net proceeds but can expedite sales. In Charlotte’s balanced market, 2-3% concessions are common to offset buyer financing hurdles without drastically affecting final profits.

What documents should Charlotte sellers prepare before settlement?

Essential items include the original deed, property tax receipts, HOA agreements (if applicable), and a paid mortgage statement. Local attorneys like Horack Talley often require a government-issued ID and recent utility bills for residency verification.

Are there strategies to minimize expenses during property transfers?

Sellers can bundle title services with preferred providers, contest high escrow fees, or opt for flat-rate legal assistance. Timing the sale to align with tax proration cycles also helps reduce out-of-pocket costs.

How does paying off an existing loan affect closing settlements?

Mortgage payoffs (including any prepayment penalties) are deducted from sale proceeds. Sellers receive remaining funds after settling balances—a process managed by closing attorneys who coordinate with lenders like Bank of America or Truist.

per 0 of sale value. Mecklenburg County adds a 0.2% local transfer tax. For a 0,000 home, sellers pay approximately

Final Thoughts on Closing Costs for Home Sellers in Charlotte

Which fees are sellers typically required to cover during a property transaction?

Sellers generally pay real estate agent commissions (5-6% of sale price), transfer taxes, title insurance premiums, and prorated property taxes. Additional costs may include attorney fees, escrow charges, and any negotiated concessions like covering buyer’s inspection fees or mortgage discount points.

How do transfer taxes function in North Carolina real estate transactions?

North Carolina imposes a statewide excise tax of $1 per $500 of sale value. Mecklenburg County adds a 0.2% local transfer tax. For a $400,000 home, sellers pay approximately $1,200 in combined state and county transfer taxes at closing.

Can commission rates be negotiated with real estate agents in Charlotte?

Yes. While 6% remains common, many Charlotte agents offer reduced rates (4-5%) for competitive listings or dual-agency situations. Sellers should compare services from firms like Allen Tate and RE/MAX when negotiating terms.

Why does title insurance matter for property transfers?

Title insurance protects against ownership disputes or liens discovered post-sale. Sellers typically pay for the owner’s policy (averaging $1,000-$2,500 in NC), which ensures clear transfer of rights and reduces legal risks for both parties.

How do concessions impact a home sale’s financial outcome?

Seller concessions—like covering repair costs or buyer’s closing fees—lower net proceeds but can expedite sales. In Charlotte’s balanced market, 2-3% concessions are common to offset buyer financing hurdles without drastically affecting final profits.

What documents should Charlotte sellers prepare before settlement?

Essential items include the original deed, property tax receipts, HOA agreements (if applicable), and a paid mortgage statement. Local attorneys like Horack Talley often require a government-issued ID and recent utility bills for residency verification.

Are there strategies to minimize expenses during property transfers?

Sellers can bundle title services with preferred providers, contest high escrow fees, or opt for flat-rate legal assistance. Timing the sale to align with tax proration cycles also helps reduce out-of-pocket costs.

How does paying off an existing loan affect closing settlements?

Mortgage payoffs (including any prepayment penalties) are deducted from sale proceeds. Sellers receive remaining funds after settling balances—a process managed by closing attorneys who coordinate with lenders like Bank of America or Truist.

,200 in combined state and county transfer taxes at closing.

Can commission rates be negotiated with real estate agents in Charlotte?

Yes. While 6% remains common, many Charlotte agents offer reduced rates (4-5%) for competitive listings or dual-agency situations. Sellers should compare services from firms like Allen Tate and RE/MAX when negotiating terms.

Why does title insurance matter for property transfers?

Title insurance protects against ownership disputes or liens discovered post-sale. Sellers typically pay for the owner’s policy (averaging

Final Thoughts on Closing Costs for Home Sellers in Charlotte

Which fees are sellers typically required to cover during a property transaction?

Sellers generally pay real estate agent commissions (5-6% of sale price), transfer taxes, title insurance premiums, and prorated property taxes. Additional costs may include attorney fees, escrow charges, and any negotiated concessions like covering buyer’s inspection fees or mortgage discount points.

How do transfer taxes function in North Carolina real estate transactions?

North Carolina imposes a statewide excise tax of $1 per $500 of sale value. Mecklenburg County adds a 0.2% local transfer tax. For a $400,000 home, sellers pay approximately $1,200 in combined state and county transfer taxes at closing.

Can commission rates be negotiated with real estate agents in Charlotte?

Yes. While 6% remains common, many Charlotte agents offer reduced rates (4-5%) for competitive listings or dual-agency situations. Sellers should compare services from firms like Allen Tate and RE/MAX when negotiating terms.

Why does title insurance matter for property transfers?

Title insurance protects against ownership disputes or liens discovered post-sale. Sellers typically pay for the owner’s policy (averaging $1,000-$2,500 in NC), which ensures clear transfer of rights and reduces legal risks for both parties.

How do concessions impact a home sale’s financial outcome?

Seller concessions—like covering repair costs or buyer’s closing fees—lower net proceeds but can expedite sales. In Charlotte’s balanced market, 2-3% concessions are common to offset buyer financing hurdles without drastically affecting final profits.

What documents should Charlotte sellers prepare before settlement?

Essential items include the original deed, property tax receipts, HOA agreements (if applicable), and a paid mortgage statement. Local attorneys like Horack Talley often require a government-issued ID and recent utility bills for residency verification.

Are there strategies to minimize expenses during property transfers?

Sellers can bundle title services with preferred providers, contest high escrow fees, or opt for flat-rate legal assistance. Timing the sale to align with tax proration cycles also helps reduce out-of-pocket costs.

How does paying off an existing loan affect closing settlements?

Mortgage payoffs (including any prepayment penalties) are deducted from sale proceeds. Sellers receive remaining funds after settling balances—a process managed by closing attorneys who coordinate with lenders like Bank of America or Truist.

,000-,500 in NC), which ensures clear transfer of rights and reduces legal risks for both parties.

How do concessions impact a home sale’s financial outcome?

Seller concessions—like covering repair costs or buyer’s closing fees—lower net proceeds but can expedite sales. In Charlotte’s balanced market, 2-3% concessions are common to offset buyer financing hurdles without drastically affecting final profits.

What documents should Charlotte sellers prepare before settlement?

Essential items include the original deed, property tax receipts, HOA agreements (if applicable), and a paid mortgage statement. Local attorneys like Horack Talley often require a government-issued ID and recent utility bills for residency verification.

Are there strategies to minimize expenses during property transfers?

Sellers can bundle title services with preferred providers, contest high escrow fees, or opt for flat-rate legal assistance. Timing the sale to align with tax proration cycles also helps reduce out-of-pocket costs.

How does paying off an existing loan affect closing settlements?

Mortgage payoffs (including any prepayment penalties) are deducted from sale proceeds. Sellers receive remaining funds after settling balances—a process managed by closing attorneys who coordinate with lenders like Bank of America or Truist.

Can commission rates be negotiated with real estate agents in Charlotte?

Why does title insurance matter for property transfers?

Final Thoughts on Closing Costs for Home Sellers in Charlotte

Which fees are sellers typically required to cover during a property transaction?

Sellers generally pay real estate agent commissions (5-6% of sale price), transfer taxes, title insurance premiums, and prorated property taxes. Additional costs may include attorney fees, escrow charges, and any negotiated concessions like covering buyer’s inspection fees or mortgage discount points.

How do transfer taxes function in North Carolina real estate transactions?

North Carolina imposes a statewide excise tax of

Final Thoughts on Closing Costs for Home Sellers in Charlotte

Which fees are sellers typically required to cover during a property transaction?

Sellers generally pay real estate agent commissions (5-6% of sale price), transfer taxes, title insurance premiums, and prorated property taxes. Additional costs may include attorney fees, escrow charges, and any negotiated concessions like covering buyer’s inspection fees or mortgage discount points.

How do transfer taxes function in North Carolina real estate transactions?

North Carolina imposes a statewide excise tax of $1 per $500 of sale value. Mecklenburg County adds a 0.2% local transfer tax. For a $400,000 home, sellers pay approximately $1,200 in combined state and county transfer taxes at closing.

Can commission rates be negotiated with real estate agents in Charlotte?

Yes. While 6% remains common, many Charlotte agents offer reduced rates (4-5%) for competitive listings or dual-agency situations. Sellers should compare services from firms like Allen Tate and RE/MAX when negotiating terms.

Why does title insurance matter for property transfers?

Title insurance protects against ownership disputes or liens discovered post-sale. Sellers typically pay for the owner’s policy (averaging $1,000-$2,500 in NC), which ensures clear transfer of rights and reduces legal risks for both parties.

How do concessions impact a home sale’s financial outcome?

Seller concessions—like covering repair costs or buyer’s closing fees—lower net proceeds but can expedite sales. In Charlotte’s balanced market, 2-3% concessions are common to offset buyer financing hurdles without drastically affecting final profits.

What documents should Charlotte sellers prepare before settlement?

Essential items include the original deed, property tax receipts, HOA agreements (if applicable), and a paid mortgage statement. Local attorneys like Horack Talley often require a government-issued ID and recent utility bills for residency verification.

Are there strategies to minimize expenses during property transfers?

Sellers can bundle title services with preferred providers, contest high escrow fees, or opt for flat-rate legal assistance. Timing the sale to align with tax proration cycles also helps reduce out-of-pocket costs.

How does paying off an existing loan affect closing settlements?

Mortgage payoffs (including any prepayment penalties) are deducted from sale proceeds. Sellers receive remaining funds after settling balances—a process managed by closing attorneys who coordinate with lenders like Bank of America or Truist.

per 0 of sale value. Mecklenburg County adds a 0.2% local transfer tax. For a 0,000 home, sellers pay approximately

Final Thoughts on Closing Costs for Home Sellers in Charlotte

Which fees are sellers typically required to cover during a property transaction?

Sellers generally pay real estate agent commissions (5-6% of sale price), transfer taxes, title insurance premiums, and prorated property taxes. Additional costs may include attorney fees, escrow charges, and any negotiated concessions like covering buyer’s inspection fees or mortgage discount points.

How do transfer taxes function in North Carolina real estate transactions?

North Carolina imposes a statewide excise tax of $1 per $500 of sale value. Mecklenburg County adds a 0.2% local transfer tax. For a $400,000 home, sellers pay approximately $1,200 in combined state and county transfer taxes at closing.

Can commission rates be negotiated with real estate agents in Charlotte?

Yes. While 6% remains common, many Charlotte agents offer reduced rates (4-5%) for competitive listings or dual-agency situations. Sellers should compare services from firms like Allen Tate and RE/MAX when negotiating terms.

Why does title insurance matter for property transfers?

Title insurance protects against ownership disputes or liens discovered post-sale. Sellers typically pay for the owner’s policy (averaging $1,000-$2,500 in NC), which ensures clear transfer of rights and reduces legal risks for both parties.

How do concessions impact a home sale’s financial outcome?

Seller concessions—like covering repair costs or buyer’s closing fees—lower net proceeds but can expedite sales. In Charlotte’s balanced market, 2-3% concessions are common to offset buyer financing hurdles without drastically affecting final profits.

What documents should Charlotte sellers prepare before settlement?

Essential items include the original deed, property tax receipts, HOA agreements (if applicable), and a paid mortgage statement. Local attorneys like Horack Talley often require a government-issued ID and recent utility bills for residency verification.

Are there strategies to minimize expenses during property transfers?

Sellers can bundle title services with preferred providers, contest high escrow fees, or opt for flat-rate legal assistance. Timing the sale to align with tax proration cycles also helps reduce out-of-pocket costs.

How does paying off an existing loan affect closing settlements?

Mortgage payoffs (including any prepayment penalties) are deducted from sale proceeds. Sellers receive remaining funds after settling balances—a process managed by closing attorneys who coordinate with lenders like Bank of America or Truist.

,200 in combined state and county transfer taxes at closing.

Can commission rates be negotiated with real estate agents in Charlotte?

Yes. While 6% remains common, many Charlotte agents offer reduced rates (4-5%) for competitive listings or dual-agency situations. Sellers should compare services from firms like Allen Tate and RE/MAX when negotiating terms.

Why does title insurance matter for property transfers?

Title insurance protects against ownership disputes or liens discovered post-sale. Sellers typically pay for the owner’s policy (averaging

Final Thoughts on Closing Costs for Home Sellers in Charlotte

Which fees are sellers typically required to cover during a property transaction?

Sellers generally pay real estate agent commissions (5-6% of sale price), transfer taxes, title insurance premiums, and prorated property taxes. Additional costs may include attorney fees, escrow charges, and any negotiated concessions like covering buyer’s inspection fees or mortgage discount points.

How do transfer taxes function in North Carolina real estate transactions?

North Carolina imposes a statewide excise tax of $1 per $500 of sale value. Mecklenburg County adds a 0.2% local transfer tax. For a $400,000 home, sellers pay approximately $1,200 in combined state and county transfer taxes at closing.

Can commission rates be negotiated with real estate agents in Charlotte?

Yes. While 6% remains common, many Charlotte agents offer reduced rates (4-5%) for competitive listings or dual-agency situations. Sellers should compare services from firms like Allen Tate and RE/MAX when negotiating terms.

Why does title insurance matter for property transfers?

Title insurance protects against ownership disputes or liens discovered post-sale. Sellers typically pay for the owner’s policy (averaging $1,000-$2,500 in NC), which ensures clear transfer of rights and reduces legal risks for both parties.

How do concessions impact a home sale’s financial outcome?

Seller concessions—like covering repair costs or buyer’s closing fees—lower net proceeds but can expedite sales. In Charlotte’s balanced market, 2-3% concessions are common to offset buyer financing hurdles without drastically affecting final profits.

What documents should Charlotte sellers prepare before settlement?

Essential items include the original deed, property tax receipts, HOA agreements (if applicable), and a paid mortgage statement. Local attorneys like Horack Talley often require a government-issued ID and recent utility bills for residency verification.

Are there strategies to minimize expenses during property transfers?

Sellers can bundle title services with preferred providers, contest high escrow fees, or opt for flat-rate legal assistance. Timing the sale to align with tax proration cycles also helps reduce out-of-pocket costs.

How does paying off an existing loan affect closing settlements?

Mortgage payoffs (including any prepayment penalties) are deducted from sale proceeds. Sellers receive remaining funds after settling balances—a process managed by closing attorneys who coordinate with lenders like Bank of America or Truist.

,000-,500 in NC), which ensures clear transfer of rights and reduces legal risks for both parties.

How do concessions impact a home sale’s financial outcome?

Seller concessions—like covering repair costs or buyer’s closing fees—lower net proceeds but can expedite sales. In Charlotte’s balanced market, 2-3% concessions are common to offset buyer financing hurdles without drastically affecting final profits.

What documents should Charlotte sellers prepare before settlement?

Essential items include the original deed, property tax receipts, HOA agreements (if applicable), and a paid mortgage statement. Local attorneys like Horack Talley often require a government-issued ID and recent utility bills for residency verification.

Are there strategies to minimize expenses during property transfers?

Sellers can bundle title services with preferred providers, contest high escrow fees, or opt for flat-rate legal assistance. Timing the sale to align with tax proration cycles also helps reduce out-of-pocket costs.

How does paying off an existing loan affect closing settlements?

Mortgage payoffs (including any prepayment penalties) are deducted from sale proceeds. Sellers receive remaining funds after settling balances—a process managed by closing attorneys who coordinate with lenders like Bank of America or Truist.

How do concessions impact a home sale’s financial outcome?

What documents should Charlotte sellers prepare before settlement?

Are there strategies to minimize expenses during property transfers?

How does paying off an existing loan affect closing settlements?

Which fees are sellers typically required to cover during a property transaction?

How do transfer taxes function in North Carolina real estate transactions?

Final Thoughts on Closing Costs for Home Sellers in Charlotte

Which fees are sellers typically required to cover during a property transaction?

Sellers generally pay real estate agent commissions (5-6% of sale price), transfer taxes, title insurance premiums, and prorated property taxes. Additional costs may include attorney fees, escrow charges, and any negotiated concessions like covering buyer’s inspection fees or mortgage discount points.

How do transfer taxes function in North Carolina real estate transactions?

North Carolina imposes a statewide excise tax of

Final Thoughts on Closing Costs for Home Sellers in Charlotte

Which fees are sellers typically required to cover during a property transaction?

Sellers generally pay real estate agent commissions (5-6% of sale price), transfer taxes, title insurance premiums, and prorated property taxes. Additional costs may include attorney fees, escrow charges, and any negotiated concessions like covering buyer’s inspection fees or mortgage discount points.

How do transfer taxes function in North Carolina real estate transactions?

North Carolina imposes a statewide excise tax of $1 per $500 of sale value. Mecklenburg County adds a 0.2% local transfer tax. For a $400,000 home, sellers pay approximately $1,200 in combined state and county transfer taxes at closing.

Can commission rates be negotiated with real estate agents in Charlotte?

Yes. While 6% remains common, many Charlotte agents offer reduced rates (4-5%) for competitive listings or dual-agency situations. Sellers should compare services from firms like Allen Tate and RE/MAX when negotiating terms.

Why does title insurance matter for property transfers?

Title insurance protects against ownership disputes or liens discovered post-sale. Sellers typically pay for the owner’s policy (averaging $1,000-$2,500 in NC), which ensures clear transfer of rights and reduces legal risks for both parties.

How do concessions impact a home sale’s financial outcome?

Seller concessions—like covering repair costs or buyer’s closing fees—lower net proceeds but can expedite sales. In Charlotte’s balanced market, 2-3% concessions are common to offset buyer financing hurdles without drastically affecting final profits.

What documents should Charlotte sellers prepare before settlement?

Essential items include the original deed, property tax receipts, HOA agreements (if applicable), and a paid mortgage statement. Local attorneys like Horack Talley often require a government-issued ID and recent utility bills for residency verification.

Are there strategies to minimize expenses during property transfers?

Sellers can bundle title services with preferred providers, contest high escrow fees, or opt for flat-rate legal assistance. Timing the sale to align with tax proration cycles also helps reduce out-of-pocket costs.

How does paying off an existing loan affect closing settlements?

Mortgage payoffs (including any prepayment penalties) are deducted from sale proceeds. Sellers receive remaining funds after settling balances—a process managed by closing attorneys who coordinate with lenders like Bank of America or Truist.

per 0 of sale value. Mecklenburg County adds a 0.2% local transfer tax. For a 0,000 home, sellers pay approximately

Final Thoughts on Closing Costs for Home Sellers in Charlotte

Which fees are sellers typically required to cover during a property transaction?

Sellers generally pay real estate agent commissions (5-6% of sale price), transfer taxes, title insurance premiums, and prorated property taxes. Additional costs may include attorney fees, escrow charges, and any negotiated concessions like covering buyer’s inspection fees or mortgage discount points.

How do transfer taxes function in North Carolina real estate transactions?

North Carolina imposes a statewide excise tax of $1 per $500 of sale value. Mecklenburg County adds a 0.2% local transfer tax. For a $400,000 home, sellers pay approximately $1,200 in combined state and county transfer taxes at closing.

Can commission rates be negotiated with real estate agents in Charlotte?

Yes. While 6% remains common, many Charlotte agents offer reduced rates (4-5%) for competitive listings or dual-agency situations. Sellers should compare services from firms like Allen Tate and RE/MAX when negotiating terms.

Why does title insurance matter for property transfers?

Title insurance protects against ownership disputes or liens discovered post-sale. Sellers typically pay for the owner’s policy (averaging $1,000-$2,500 in NC), which ensures clear transfer of rights and reduces legal risks for both parties.

How do concessions impact a home sale’s financial outcome?

Seller concessions—like covering repair costs or buyer’s closing fees—lower net proceeds but can expedite sales. In Charlotte’s balanced market, 2-3% concessions are common to offset buyer financing hurdles without drastically affecting final profits.

What documents should Charlotte sellers prepare before settlement?

Essential items include the original deed, property tax receipts, HOA agreements (if applicable), and a paid mortgage statement. Local attorneys like Horack Talley often require a government-issued ID and recent utility bills for residency verification.

Are there strategies to minimize expenses during property transfers?

Sellers can bundle title services with preferred providers, contest high escrow fees, or opt for flat-rate legal assistance. Timing the sale to align with tax proration cycles also helps reduce out-of-pocket costs.

How does paying off an existing loan affect closing settlements?

Mortgage payoffs (including any prepayment penalties) are deducted from sale proceeds. Sellers receive remaining funds after settling balances—a process managed by closing attorneys who coordinate with lenders like Bank of America or Truist.

,200 in combined state and county transfer taxes at closing.

Can commission rates be negotiated with real estate agents in Charlotte?

Yes. While 6% remains common, many Charlotte agents offer reduced rates (4-5%) for competitive listings or dual-agency situations. Sellers should compare services from firms like Allen Tate and RE/MAX when negotiating terms.

Why does title insurance matter for property transfers?

Title insurance protects against ownership disputes or liens discovered post-sale. Sellers typically pay for the owner’s policy (averaging

Final Thoughts on Closing Costs for Home Sellers in Charlotte

Which fees are sellers typically required to cover during a property transaction?

Sellers generally pay real estate agent commissions (5-6% of sale price), transfer taxes, title insurance premiums, and prorated property taxes. Additional costs may include attorney fees, escrow charges, and any negotiated concessions like covering buyer’s inspection fees or mortgage discount points.

How do transfer taxes function in North Carolina real estate transactions?

North Carolina imposes a statewide excise tax of $1 per $500 of sale value. Mecklenburg County adds a 0.2% local transfer tax. For a $400,000 home, sellers pay approximately $1,200 in combined state and county transfer taxes at closing.

Can commission rates be negotiated with real estate agents in Charlotte?

Yes. While 6% remains common, many Charlotte agents offer reduced rates (4-5%) for competitive listings or dual-agency situations. Sellers should compare services from firms like Allen Tate and RE/MAX when negotiating terms.

Why does title insurance matter for property transfers?

Title insurance protects against ownership disputes or liens discovered post-sale. Sellers typically pay for the owner’s policy (averaging $1,000-$2,500 in NC), which ensures clear transfer of rights and reduces legal risks for both parties.

How do concessions impact a home sale’s financial outcome?

Seller concessions—like covering repair costs or buyer’s closing fees—lower net proceeds but can expedite sales. In Charlotte’s balanced market, 2-3% concessions are common to offset buyer financing hurdles without drastically affecting final profits.

What documents should Charlotte sellers prepare before settlement?

Essential items include the original deed, property tax receipts, HOA agreements (if applicable), and a paid mortgage statement. Local attorneys like Horack Talley often require a government-issued ID and recent utility bills for residency verification.

Are there strategies to minimize expenses during property transfers?

Sellers can bundle title services with preferred providers, contest high escrow fees, or opt for flat-rate legal assistance. Timing the sale to align with tax proration cycles also helps reduce out-of-pocket costs.

How does paying off an existing loan affect closing settlements?

Mortgage payoffs (including any prepayment penalties) are deducted from sale proceeds. Sellers receive remaining funds after settling balances—a process managed by closing attorneys who coordinate with lenders like Bank of America or Truist.

,000-,500 in NC), which ensures clear transfer of rights and reduces legal risks for both parties.

How do concessions impact a home sale’s financial outcome?

Seller concessions—like covering repair costs or buyer’s closing fees—lower net proceeds but can expedite sales. In Charlotte’s balanced market, 2-3% concessions are common to offset buyer financing hurdles without drastically affecting final profits.

What documents should Charlotte sellers prepare before settlement?

Essential items include the original deed, property tax receipts, HOA agreements (if applicable), and a paid mortgage statement. Local attorneys like Horack Talley often require a government-issued ID and recent utility bills for residency verification.

Are there strategies to minimize expenses during property transfers?

Sellers can bundle title services with preferred providers, contest high escrow fees, or opt for flat-rate legal assistance. Timing the sale to align with tax proration cycles also helps reduce out-of-pocket costs.

How does paying off an existing loan affect closing settlements?

Mortgage payoffs (including any prepayment penalties) are deducted from sale proceeds. Sellers receive remaining funds after settling balances—a process managed by closing attorneys who coordinate with lenders like Bank of America or Truist.

Final Thoughts on Closing Costs for Home Sellers in Charlotte

Which fees are sellers typically required to cover during a property transaction?

Sellers generally pay real estate agent commissions (5-6% of sale price), transfer taxes, title insurance premiums, and prorated property taxes. Additional costs may include attorney fees, escrow charges, and any negotiated concessions like covering buyer’s inspection fees or mortgage discount points.

How do transfer taxes function in North Carolina real estate transactions?

North Carolina imposes a statewide excise tax of

Final Thoughts on Closing Costs for Home Sellers in Charlotte

Which fees are sellers typically required to cover during a property transaction?

Sellers generally pay real estate agent commissions (5-6% of sale price), transfer taxes, title insurance premiums, and prorated property taxes. Additional costs may include attorney fees, escrow charges, and any negotiated concessions like covering buyer’s inspection fees or mortgage discount points.

How do transfer taxes function in North Carolina real estate transactions?

North Carolina imposes a statewide excise tax of $1 per $500 of sale value. Mecklenburg County adds a 0.2% local transfer tax. For a $400,000 home, sellers pay approximately $1,200 in combined state and county transfer taxes at closing.

Can commission rates be negotiated with real estate agents in Charlotte?

Yes. While 6% remains common, many Charlotte agents offer reduced rates (4-5%) for competitive listings or dual-agency situations. Sellers should compare services from firms like Allen Tate and RE/MAX when negotiating terms.

Why does title insurance matter for property transfers?

Title insurance protects against ownership disputes or liens discovered post-sale. Sellers typically pay for the owner’s policy (averaging $1,000-$2,500 in NC), which ensures clear transfer of rights and reduces legal risks for both parties.

How do concessions impact a home sale’s financial outcome?

Seller concessions—like covering repair costs or buyer’s closing fees—lower net proceeds but can expedite sales. In Charlotte’s balanced market, 2-3% concessions are common to offset buyer financing hurdles without drastically affecting final profits.

What documents should Charlotte sellers prepare before settlement?

Essential items include the original deed, property tax receipts, HOA agreements (if applicable), and a paid mortgage statement. Local attorneys like Horack Talley often require a government-issued ID and recent utility bills for residency verification.

Are there strategies to minimize expenses during property transfers?

Sellers can bundle title services with preferred providers, contest high escrow fees, or opt for flat-rate legal assistance. Timing the sale to align with tax proration cycles also helps reduce out-of-pocket costs.

How does paying off an existing loan affect closing settlements?

Mortgage payoffs (including any prepayment penalties) are deducted from sale proceeds. Sellers receive remaining funds after settling balances—a process managed by closing attorneys who coordinate with lenders like Bank of America or Truist.

per 0 of sale value. Mecklenburg County adds a 0.2% local transfer tax. For a 0,000 home, sellers pay approximately

Final Thoughts on Closing Costs for Home Sellers in Charlotte

Which fees are sellers typically required to cover during a property transaction?

Sellers generally pay real estate agent commissions (5-6% of sale price), transfer taxes, title insurance premiums, and prorated property taxes. Additional costs may include attorney fees, escrow charges, and any negotiated concessions like covering buyer’s inspection fees or mortgage discount points.

How do transfer taxes function in North Carolina real estate transactions?

North Carolina imposes a statewide excise tax of $1 per $500 of sale value. Mecklenburg County adds a 0.2% local transfer tax. For a $400,000 home, sellers pay approximately $1,200 in combined state and county transfer taxes at closing.

Can commission rates be negotiated with real estate agents in Charlotte?

Yes. While 6% remains common, many Charlotte agents offer reduced rates (4-5%) for competitive listings or dual-agency situations. Sellers should compare services from firms like Allen Tate and RE/MAX when negotiating terms.

Why does title insurance matter for property transfers?

Title insurance protects against ownership disputes or liens discovered post-sale. Sellers typically pay for the owner’s policy (averaging $1,000-$2,500 in NC), which ensures clear transfer of rights and reduces legal risks for both parties.

How do concessions impact a home sale’s financial outcome?

Seller concessions—like covering repair costs or buyer’s closing fees—lower net proceeds but can expedite sales. In Charlotte’s balanced market, 2-3% concessions are common to offset buyer financing hurdles without drastically affecting final profits.

What documents should Charlotte sellers prepare before settlement?

Essential items include the original deed, property tax receipts, HOA agreements (if applicable), and a paid mortgage statement. Local attorneys like Horack Talley often require a government-issued ID and recent utility bills for residency verification.

Are there strategies to minimize expenses during property transfers?

Sellers can bundle title services with preferred providers, contest high escrow fees, or opt for flat-rate legal assistance. Timing the sale to align with tax proration cycles also helps reduce out-of-pocket costs.

How does paying off an existing loan affect closing settlements?

Mortgage payoffs (including any prepayment penalties) are deducted from sale proceeds. Sellers receive remaining funds after settling balances—a process managed by closing attorneys who coordinate with lenders like Bank of America or Truist.

,200 in combined state and county transfer taxes at closing.

Can commission rates be negotiated with real estate agents in Charlotte?

Yes. While 6% remains common, many Charlotte agents offer reduced rates (4-5%) for competitive listings or dual-agency situations. Sellers should compare services from firms like Allen Tate and RE/MAX when negotiating terms.

Why does title insurance matter for property transfers?

Title insurance protects against ownership disputes or liens discovered post-sale. Sellers typically pay for the owner’s policy (averaging

Final Thoughts on Closing Costs for Home Sellers in Charlotte

Which fees are sellers typically required to cover during a property transaction?

Sellers generally pay real estate agent commissions (5-6% of sale price), transfer taxes, title insurance premiums, and prorated property taxes. Additional costs may include attorney fees, escrow charges, and any negotiated concessions like covering buyer’s inspection fees or mortgage discount points.

How do transfer taxes function in North Carolina real estate transactions?

North Carolina imposes a statewide excise tax of $1 per $500 of sale value. Mecklenburg County adds a 0.2% local transfer tax. For a $400,000 home, sellers pay approximately $1,200 in combined state and county transfer taxes at closing.

Can commission rates be negotiated with real estate agents in Charlotte?

Yes. While 6% remains common, many Charlotte agents offer reduced rates (4-5%) for competitive listings or dual-agency situations. Sellers should compare services from firms like Allen Tate and RE/MAX when negotiating terms.

Why does title insurance matter for property transfers?

Title insurance protects against ownership disputes or liens discovered post-sale. Sellers typically pay for the owner’s policy (averaging $1,000-$2,500 in NC), which ensures clear transfer of rights and reduces legal risks for both parties.

How do concessions impact a home sale’s financial outcome?

Seller concessions—like covering repair costs or buyer’s closing fees—lower net proceeds but can expedite sales. In Charlotte’s balanced market, 2-3% concessions are common to offset buyer financing hurdles without drastically affecting final profits.

What documents should Charlotte sellers prepare before settlement?

Essential items include the original deed, property tax receipts, HOA agreements (if applicable), and a paid mortgage statement. Local attorneys like Horack Talley often require a government-issued ID and recent utility bills for residency verification.

Are there strategies to minimize expenses during property transfers?

Sellers can bundle title services with preferred providers, contest high escrow fees, or opt for flat-rate legal assistance. Timing the sale to align with tax proration cycles also helps reduce out-of-pocket costs.

How does paying off an existing loan affect closing settlements?

Mortgage payoffs (including any prepayment penalties) are deducted from sale proceeds. Sellers receive remaining funds after settling balances—a process managed by closing attorneys who coordinate with lenders like Bank of America or Truist.

,000-,500 in NC), which ensures clear transfer of rights and reduces legal risks for both parties.

How do concessions impact a home sale’s financial outcome?

Seller concessions—like covering repair costs or buyer’s closing fees—lower net proceeds but can expedite sales. In Charlotte’s balanced market, 2-3% concessions are common to offset buyer financing hurdles without drastically affecting final profits.

What documents should Charlotte sellers prepare before settlement?

Essential items include the original deed, property tax receipts, HOA agreements (if applicable), and a paid mortgage statement. Local attorneys like Horack Talley often require a government-issued ID and recent utility bills for residency verification.

Are there strategies to minimize expenses during property transfers?

Sellers can bundle title services with preferred providers, contest high escrow fees, or opt for flat-rate legal assistance. Timing the sale to align with tax proration cycles also helps reduce out-of-pocket costs.

How does paying off an existing loan affect closing settlements?

Mortgage payoffs (including any prepayment penalties) are deducted from sale proceeds. Sellers receive remaining funds after settling balances—a process managed by closing attorneys who coordinate with lenders like Bank of America or Truist.

Can commission rates be negotiated with real estate agents in Charlotte?

Why does title insurance matter for property transfers?

Final Thoughts on Closing Costs for Home Sellers in Charlotte

Which fees are sellers typically required to cover during a property transaction?

Sellers generally pay real estate agent commissions (5-6% of sale price), transfer taxes, title insurance premiums, and prorated property taxes. Additional costs may include attorney fees, escrow charges, and any negotiated concessions like covering buyer’s inspection fees or mortgage discount points.

How do transfer taxes function in North Carolina real estate transactions?

North Carolina imposes a statewide excise tax of

Final Thoughts on Closing Costs for Home Sellers in Charlotte

Which fees are sellers typically required to cover during a property transaction?

Sellers generally pay real estate agent commissions (5-6% of sale price), transfer taxes, title insurance premiums, and prorated property taxes. Additional costs may include attorney fees, escrow charges, and any negotiated concessions like covering buyer’s inspection fees or mortgage discount points.

How do transfer taxes function in North Carolina real estate transactions?

North Carolina imposes a statewide excise tax of $1 per $500 of sale value. Mecklenburg County adds a 0.2% local transfer tax. For a $400,000 home, sellers pay approximately $1,200 in combined state and county transfer taxes at closing.

Can commission rates be negotiated with real estate agents in Charlotte?

Yes. While 6% remains common, many Charlotte agents offer reduced rates (4-5%) for competitive listings or dual-agency situations. Sellers should compare services from firms like Allen Tate and RE/MAX when negotiating terms.

Why does title insurance matter for property transfers?

Title insurance protects against ownership disputes or liens discovered post-sale. Sellers typically pay for the owner’s policy (averaging $1,000-$2,500 in NC), which ensures clear transfer of rights and reduces legal risks for both parties.

How do concessions impact a home sale’s financial outcome?

Seller concessions—like covering repair costs or buyer’s closing fees—lower net proceeds but can expedite sales. In Charlotte’s balanced market, 2-3% concessions are common to offset buyer financing hurdles without drastically affecting final profits.

What documents should Charlotte sellers prepare before settlement?

Essential items include the original deed, property tax receipts, HOA agreements (if applicable), and a paid mortgage statement. Local attorneys like Horack Talley often require a government-issued ID and recent utility bills for residency verification.

Are there strategies to minimize expenses during property transfers?

Sellers can bundle title services with preferred providers, contest high escrow fees, or opt for flat-rate legal assistance. Timing the sale to align with tax proration cycles also helps reduce out-of-pocket costs.

How does paying off an existing loan affect closing settlements?

Mortgage payoffs (including any prepayment penalties) are deducted from sale proceeds. Sellers receive remaining funds after settling balances—a process managed by closing attorneys who coordinate with lenders like Bank of America or Truist.

per 0 of sale value. Mecklenburg County adds a 0.2% local transfer tax. For a 0,000 home, sellers pay approximately

Final Thoughts on Closing Costs for Home Sellers in Charlotte

Which fees are sellers typically required to cover during a property transaction?

Sellers generally pay real estate agent commissions (5-6% of sale price), transfer taxes, title insurance premiums, and prorated property taxes. Additional costs may include attorney fees, escrow charges, and any negotiated concessions like covering buyer’s inspection fees or mortgage discount points.

How do transfer taxes function in North Carolina real estate transactions?

North Carolina imposes a statewide excise tax of $1 per $500 of sale value. Mecklenburg County adds a 0.2% local transfer tax. For a $400,000 home, sellers pay approximately $1,200 in combined state and county transfer taxes at closing.

Can commission rates be negotiated with real estate agents in Charlotte?

Yes. While 6% remains common, many Charlotte agents offer reduced rates (4-5%) for competitive listings or dual-agency situations. Sellers should compare services from firms like Allen Tate and RE/MAX when negotiating terms.

Why does title insurance matter for property transfers?

Title insurance protects against ownership disputes or liens discovered post-sale. Sellers typically pay for the owner’s policy (averaging $1,000-$2,500 in NC), which ensures clear transfer of rights and reduces legal risks for both parties.

How do concessions impact a home sale’s financial outcome?

Seller concessions—like covering repair costs or buyer’s closing fees—lower net proceeds but can expedite sales. In Charlotte’s balanced market, 2-3% concessions are common to offset buyer financing hurdles without drastically affecting final profits.

What documents should Charlotte sellers prepare before settlement?

Essential items include the original deed, property tax receipts, HOA agreements (if applicable), and a paid mortgage statement. Local attorneys like Horack Talley often require a government-issued ID and recent utility bills for residency verification.

Are there strategies to minimize expenses during property transfers?

Sellers can bundle title services with preferred providers, contest high escrow fees, or opt for flat-rate legal assistance. Timing the sale to align with tax proration cycles also helps reduce out-of-pocket costs.

How does paying off an existing loan affect closing settlements?

Mortgage payoffs (including any prepayment penalties) are deducted from sale proceeds. Sellers receive remaining funds after settling balances—a process managed by closing attorneys who coordinate with lenders like Bank of America or Truist.

,200 in combined state and county transfer taxes at closing.

Can commission rates be negotiated with real estate agents in Charlotte?

Yes. While 6% remains common, many Charlotte agents offer reduced rates (4-5%) for competitive listings or dual-agency situations. Sellers should compare services from firms like Allen Tate and RE/MAX when negotiating terms.

Why does title insurance matter for property transfers?

Title insurance protects against ownership disputes or liens discovered post-sale. Sellers typically pay for the owner’s policy (averaging

Final Thoughts on Closing Costs for Home Sellers in Charlotte

Which fees are sellers typically required to cover during a property transaction?

Sellers generally pay real estate agent commissions (5-6% of sale price), transfer taxes, title insurance premiums, and prorated property taxes. Additional costs may include attorney fees, escrow charges, and any negotiated concessions like covering buyer’s inspection fees or mortgage discount points.

How do transfer taxes function in North Carolina real estate transactions?

North Carolina imposes a statewide excise tax of $1 per $500 of sale value. Mecklenburg County adds a 0.2% local transfer tax. For a $400,000 home, sellers pay approximately $1,200 in combined state and county transfer taxes at closing.

Can commission rates be negotiated with real estate agents in Charlotte?

Yes. While 6% remains common, many Charlotte agents offer reduced rates (4-5%) for competitive listings or dual-agency situations. Sellers should compare services from firms like Allen Tate and RE/MAX when negotiating terms.

Why does title insurance matter for property transfers?

Title insurance protects against ownership disputes or liens discovered post-sale. Sellers typically pay for the owner’s policy (averaging $1,000-$2,500 in NC), which ensures clear transfer of rights and reduces legal risks for both parties.

How do concessions impact a home sale’s financial outcome?

Seller concessions—like covering repair costs or buyer’s closing fees—lower net proceeds but can expedite sales. In Charlotte’s balanced market, 2-3% concessions are common to offset buyer financing hurdles without drastically affecting final profits.

What documents should Charlotte sellers prepare before settlement?

Essential items include the original deed, property tax receipts, HOA agreements (if applicable), and a paid mortgage statement. Local attorneys like Horack Talley often require a government-issued ID and recent utility bills for residency verification.

Are there strategies to minimize expenses during property transfers?

Sellers can bundle title services with preferred providers, contest high escrow fees, or opt for flat-rate legal assistance. Timing the sale to align with tax proration cycles also helps reduce out-of-pocket costs.

How does paying off an existing loan affect closing settlements?

Mortgage payoffs (including any prepayment penalties) are deducted from sale proceeds. Sellers receive remaining funds after settling balances—a process managed by closing attorneys who coordinate with lenders like Bank of America or Truist.