When mortgage payments fall behind, homeowners in Charlotte face a structured series of steps. Understanding this sequence helps you make informed decisions. Local experts like Clients 1st Property Group (704-622-4865) emphasize that knowledge is power during these situations.

Every case begins with a missed payment. After several months of non-payment, lenders typically initiate formal action. North Carolina laws shape how quickly this unfolds, with timelines varying based on loan terms and property type. Some cases involve court oversight, while others follow alternative paths.

This guide breaks down each phase clearly. You’ll learn about notices, redemption periods, and potential outcomes. We’ve compiled current data from Charlotte’s real estate landscape to ensure accuracy. Whether you’re exploring options or preparing for next steps, actionable insights await.

Key Takeaways

- North Carolina foreclosure rules differ from other states

- Initial missed payments trigger lender communication

- Two primary methods exist: court-supervised and alternative paths

- Local market conditions impact resolution strategies

- Professional guidance helps navigate complex scenarios

Understanding the Foreclosure Process in Charlotte

Mortgage difficulties can quickly escalate into complex legal scenarios for Charlotte residents. When multiple payments remain overdue, lenders may pursue recovery actions under state guidelines. Clients 1st Property Group (704-622-4865) specializes in helping families navigate these sensitive situations with tailored strategies.

Defining the Legal Journey

A mortgage default occurs after 90-120 days of missed payments. This triggers formal communication from lenders, including a demand letter and Notice of Default. North Carolina requires lenders to file documents with local courts, initiating structured recovery procedures.

Consequences for Property Owners

The financial strain often creates emotional stress and impacts credit scores for 7+ years. Homeowners risk losing their property through public auctions if resolutions aren’t reached. Clients 1st Property Group notes:

“Early intervention preserves more options than last-minute decisions.”

Local regulations allow a 10-day grace period after initial notices before further action. Understanding these windows helps families explore alternatives like loan modifications or repayment plans. Professional guidance often reveals paths not immediately apparent in stressful situations.

Foreclosure Process Timeline: A Step-by-Step Guide

Navigating mortgage challenges requires understanding key milestones. Charlotte homeowners often benefit from visualizing the sequence of events that follow missed payments. This structured approach helps identify critical decision points.

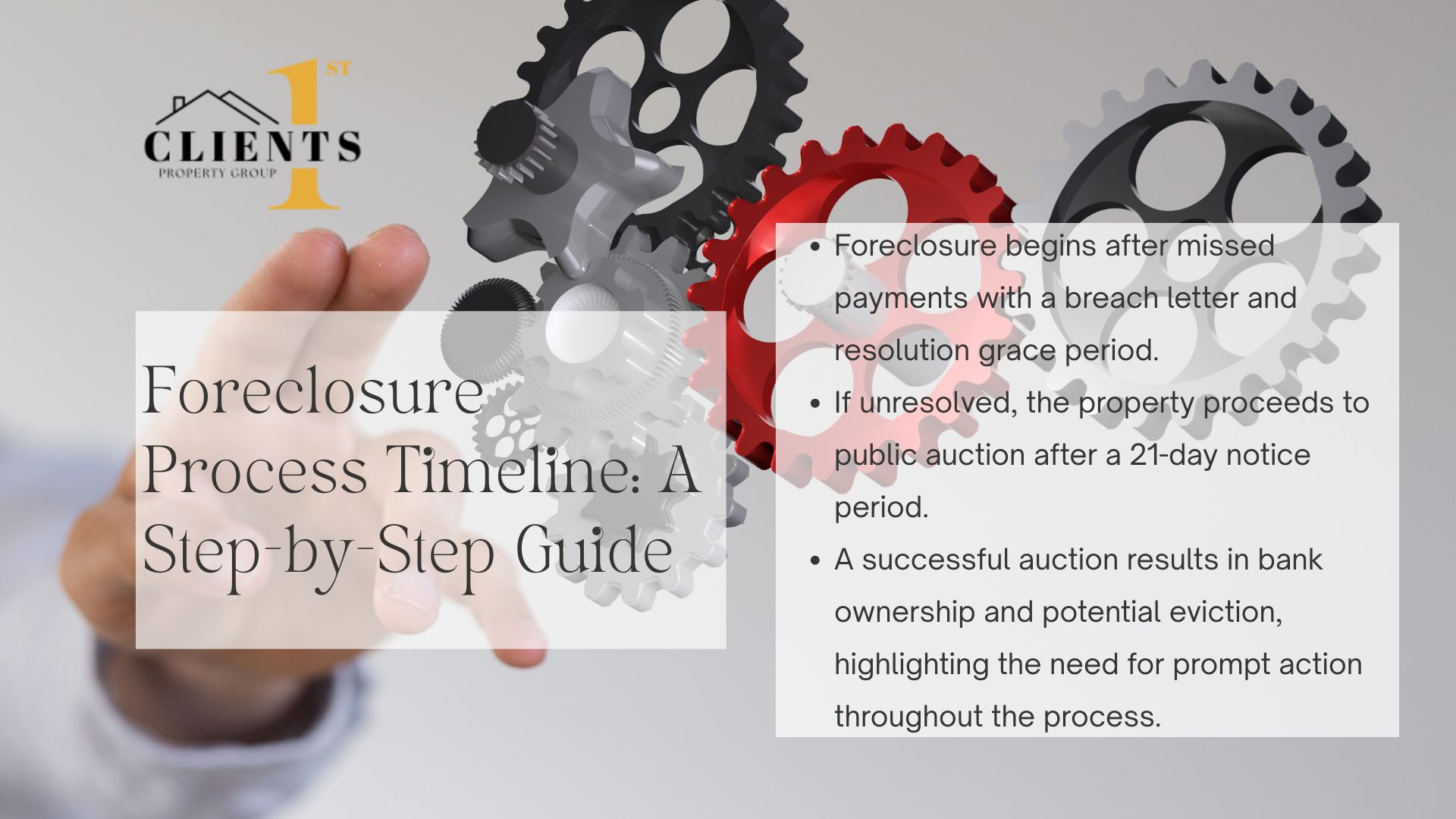

Payment Default & Notice Phase

After three consecutive missed payments, lenders typically issue a formal breach letter. North Carolina law mandates a 10-day grace period for resolution. During this window, homeowners can:

- Negotiate repayment plans

- Explore loan modifications

- Seek legal counsel

| Stage | Typical Duration | Lender Actions | Homeowner Options |

|---|---|---|---|

| Initial Default | 90-120 days | Send reminders | Contact housing counselor |

| Notice of Default | 10 days | File court documents | Submit cure payment |

| Auction Notice | 21 days | Publish sale details | Request mediation |

Foreclosure Sale and Eviction

If unresolved, properties enter public auction 21 days after final notices. Successful bids convert homes to REO (bank-owned) status. Unsuccessful auctions may lead to:

- Price reductions

- Private negotiations

- Alternative sales

One lender representative states:

“Responding promptly to notices preserves more options than waiting until deadlines.”

Post-sale evictions generally occur within 30 days in Charlotte. Local courts require proper documentation before authorizing property possession changes.

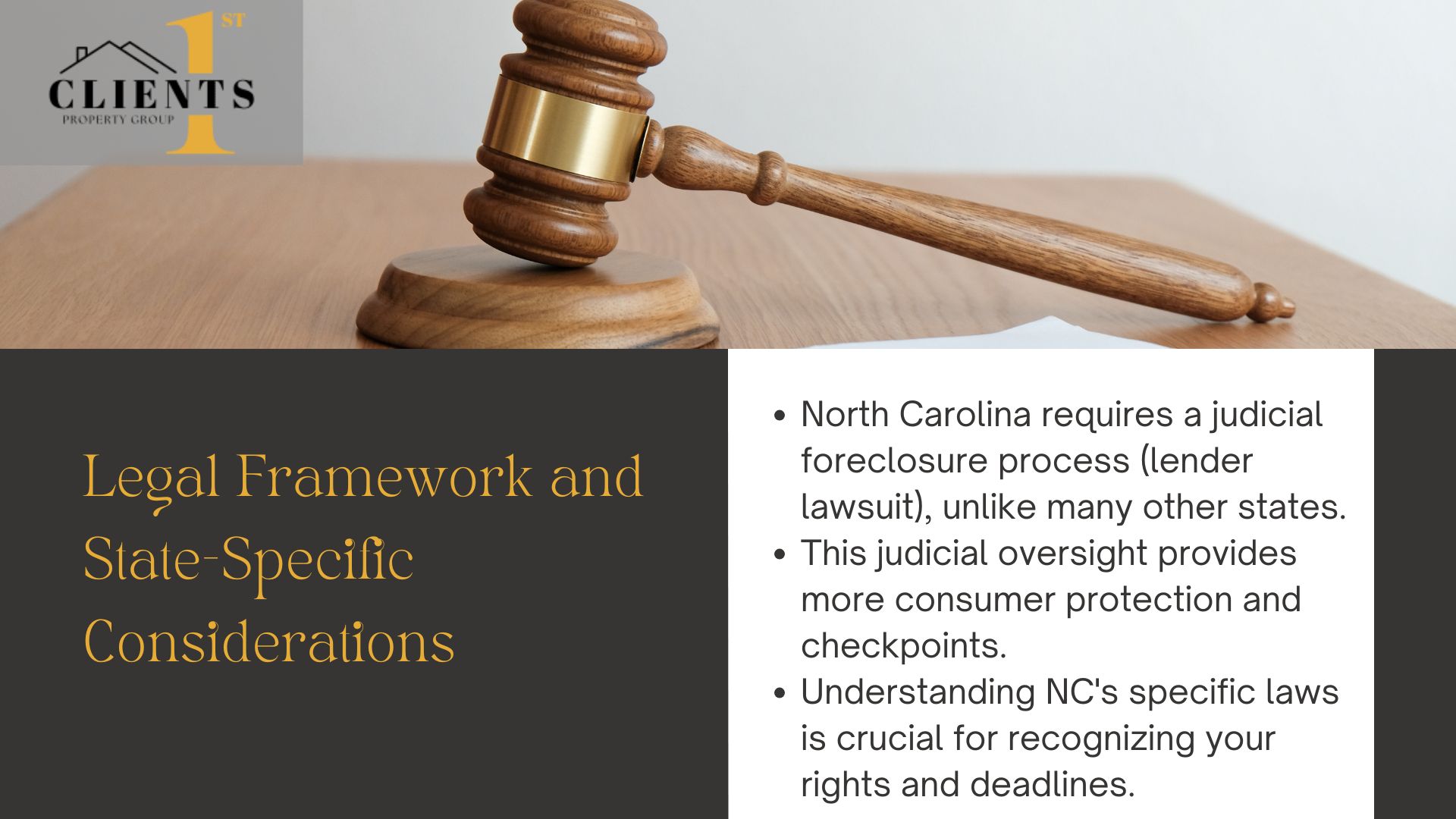

Legal Framework and State-Specific Considerations

State laws significantly influence how property challenges unfold, making local legal knowledge essential for homeowners. North Carolina’s approach differs from many states, particularly in how lenders address mortgage defaults. Understanding these distinctions helps you recognize rights and deadlines that could alter outcomes.

North Carolina Foreclosure Laws

North Carolina operates under strict judicial oversight for most property recoveries. Unlike some states allowing non-court procedures, lenders must file a lawsuit to initiate action here. This ensures court review of documentation before approving auctions. Key features include:

- Mandatory 10-day response period after initial notices

- Public auctions supervised by county trustees

- Redemption rights limited to specific scenarios

Judicial vs Non-Judicial Processes

Judicial foreclosure requires court approval at every stage, adding layers of consumer protection. Non-judicial paths, permitted in 30+ states, let lenders act without lawsuits if contracts include “power of sale” clauses. North Carolina rarely allows this method, prioritizing judicial review. A Charlotte real estate attorney notes:

“The court’s involvement here creates critical checkpoints homeowners can use to explore alternatives.”

| Process Type | Court Involvement | Timeline | Homeowner Rights |

|---|---|---|---|

| Judicial | Required | 4-8 months | Formal dispute options |

| Non-Judicial | Minimal | 2-4 months | Limited objections |

State variations matter greatly. For example, neighboring South Carolina permits non-judicial methods under certain conditions. Always verify local regulations when facing payment difficulties.

Exploring Loss Mitigation and Homeowner Options

Charlotte homeowners facing financial hurdles have multiple paths to avoid losing their property. Loss mitigation strategies can pause or reduce payments while exploring long-term solutions. These options often require proactive communication with lenders and documented financial hardship.

Forbearance and Mediation Strategies

A forbearance agreement temporarily pauses or reduces mortgage payments. Lenders typically require proof of income changes or medical emergencies. Successful cases show these steps help:

- Submit hardship letter within 30 days of default

- Provide bank statements and tax documents

- Attend free housing counseling sessions

Mediation programs in Mecklenburg County let homeowners negotiate modified terms. A housing counselor notes:

“Mediation success rates jump 62% when participants bring organized financial records.”

| Strategy | Duration | Impact on Credit |

|---|---|---|

| Forbearance | 3-12 months | Minor temporary dip |

| Mediation | 60-90 days | No direct effect |

Short Sale and Deed in Lieu Alternatives

A short sale lets homeowners sell their home below market value with lender approval. This avoids public auction but requires:

- Proof the sale price covers lender costs

- No junior liens on the property

- Full disclosure of financial status

Deed in lieu transfers ownership directly to the lender. While faster than foreclosure, it may involve tax implications. The Smith family in Charlotte avoided credit damage by completing a deed in lieu with a structured agreement.

Trust proceedings often govern short sale approvals. Lenders prioritize these alternatives when homeowners act before the notice sale period ends. Timely action preserves negotiation leverage and equity retention.

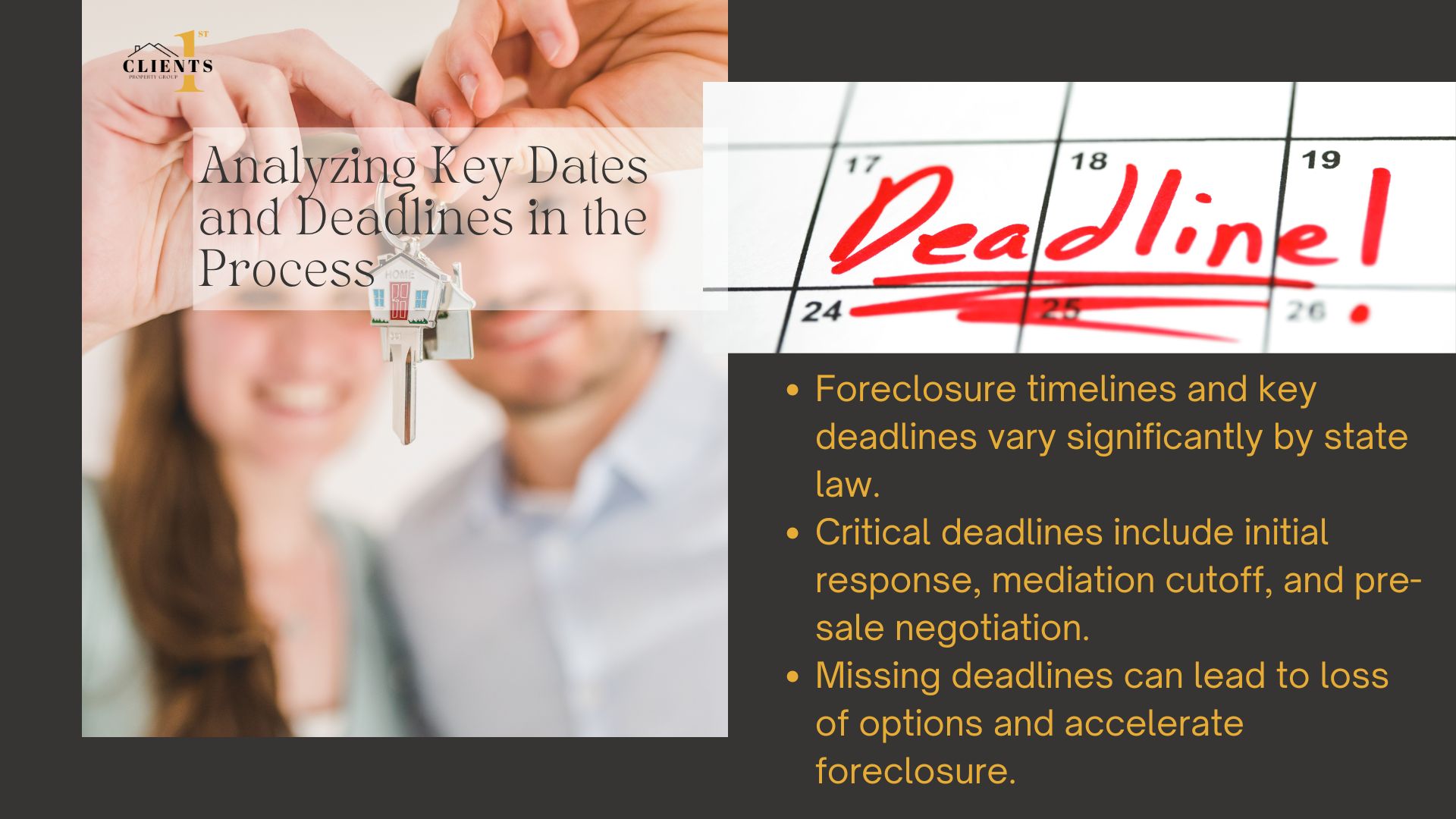

Analyzing Key Dates and Deadlines in the Process

Missing key deadlines can drastically alter outcomes for property owners. State laws create varying windows for action, making awareness essential. Tracking critical dates helps maintain control during challenging financial situations.

Timeline Variations by State

Legal frameworks differ significantly across state lines. North Carolina allows 10 days to respond after initial notices, while Texas grants 20 days. California requires lenders to wait 120 days before filing. These differences impact strategies for resolution.

| State | Grace Period | Mediation Window | Auction Notice |

|---|---|---|---|

| NC | 10 days | 30 days | 21 days pre-sale |

| TX | 20 days | 45 days | 30 days pre-sale |

| CA | 30 days | 60 days | 20 days pre-sale |

Critical Legal Deadlines

Three dates demand immediate attention:

- Initial notice response window (10-30 days)

- Mediation request cutoff (varies by county)

- Pre-sale negotiation period (21-45 days)

A Charlotte attorney emphasizes:

“Missing the 10-day response deadline in North Carolina often eliminates mediation opportunities.”

Track deadlines using digital calendars or professional services. Set multiple reminders for each phase. Late submissions can accelerate property loss by 2-4 months in most states.

How Foreclosure Affects Property Value and Future Mortgages

The financial ripple effects of unresolved mortgage issues extend far beyond initial challenges. Property values in affected neighborhoods often dip by 5-15% post-sale, according to recent Charlotte market analyses. These impacts can linger for 2-3 years, creating hurdles for both former owners and surrounding residents.

Long-Term Impacts on Credit

A completed home foreclosure typically lowers credit scores by 150-200 points. This damage remains visible for 7 years, though its severity lessens over time. Recent studies show:

- 50% of affected borrowers qualify for new loans within 3-5 years

- FHA mortgage eligibility resumes after 3 years with improved credit

- Conventional loans require 7-year waiting periods

| Time After Foreclosure | Average Credit Score | Mortgage Eligibility |

|---|---|---|

| 1 Year | 550-600 | Limited Options |

| 3 Years | 620-670 | FHA/VA Loans |

| 7 Years | 680+ | Conventional Loans |

Advice for Rebuilding Financial Stability

Rebuilding starts with strategic financial planning. Experts recommend these steps:

- Establish automatic savings for emergency funds

- Use secured credit cards to rebuild payment history

- Monitor credit reports quarterly for errors

A Charlotte financial advisor notes:

“Consistent, small improvements create better results than drastic overhauls. Focus on steady progress rather than perfection.”

State-specific programs in North Carolina offer credit counseling grants for qualifying residents. Partnering with housing nonprofits often reveals local resources not widely advertised. With disciplined effort, most borrowers restore their financial health within 5-7 years.

Contacting Clients 1st Property Group for Expert Assistance

Facing financial uncertainty with your home can feel overwhelming. Clients 1st Property Group offers tailored solutions to help Charlotte residents navigate complex situations. Their team provides clear guidance while respecting your unique circumstances.

Local Expertise at Your Service

The Charlotte office (704-622-4865) connects homeowners with specialists who understand local regulations. Their advisors help interpret lender communications and identify practical next steps. Common services include:

- Reviewing legal notices for accuracy

- Negotiating with financial institutions

- Exploring alternative agreements

| Service | Benefit | Timeframe |

|---|---|---|

| Initial Consultation | Clarify options | 24-48 hours |

| Lender Negotiation | Reduce stress | 1-3 weeks |

| Document Review | Avoid errors | Same day |

Personalized Support When It Matters

One team member shares:

“We prioritize understanding each family’s situation before suggesting solutions. Every case deserves individual attention.”

Homeowners appreciate their transparent approach to challenging conversations. Whether facing initial notices or complex negotiations, proactive communication often reveals unexpected paths forward.

- Office: Charlotte, North Carolina

- Phone: (704) 622-4865

- Availability: Weekdays 8 AM – 6 PM ET

Conclusion

Facing mortgage challenges in Charlotte demands awareness of legal safeguards and response windows. State laws shape every phase, from initial notice requirements to final sale procedures. Missing critical deadlines can accelerate property loss, while timely action preserves negotiation opportunities.

Understanding default notices and lender obligations helps homeowners explore alternatives like repayment plans or mediation. North Carolina’s judicial oversight adds protection layers, but requires strict adherence to court timelines. Local experts at Clients 1st Property Group (704-622-4865) decode complex scenarios into actionable steps.

Proactive strategies reduce long-term financial impacts. Whether pursuing loan modifications or considering a short sale, informed decisions protect both your home and credit health. Reach out for guidance before deadlines expire – early intervention often yields better outcomes than last-minute efforts.

Knowledge transforms uncertainty into manageable steps. With Charlotte-specific insights and professional support, you can navigate these challenges while safeguarding your future stability.